The Middle East AI Economy is Facing Its First Stress Test

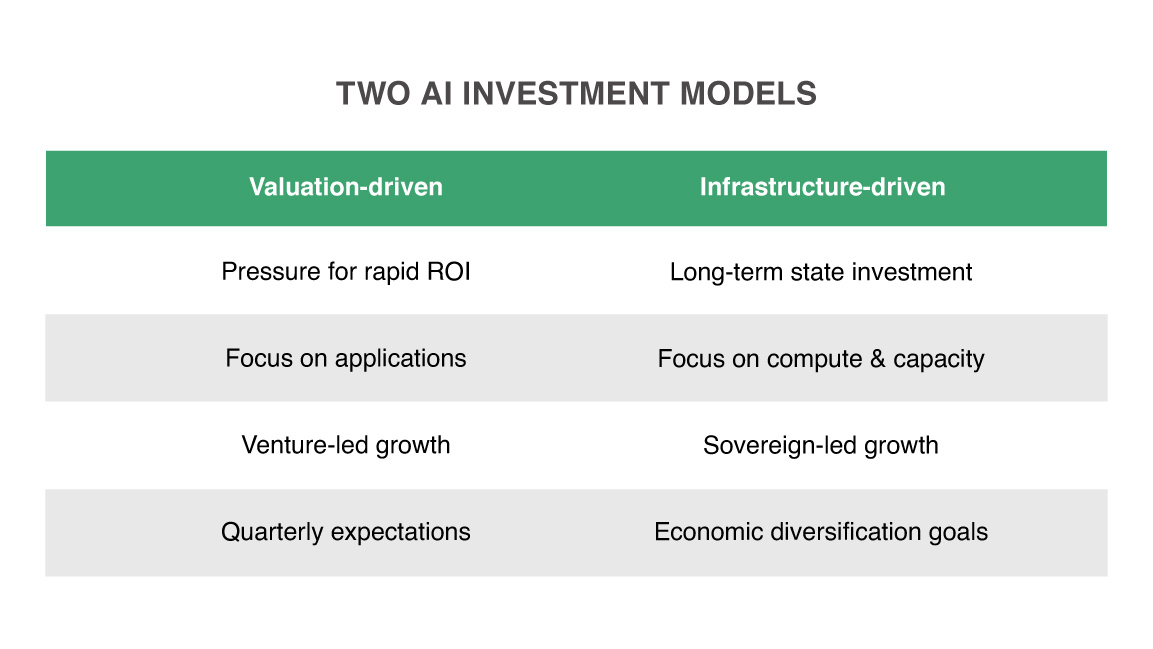

The Gulf's AI strategy—grounded in sovereign capital and long-term infrastructure—reminds us that resilience, not just innovation speed, is becoming a defining competitive advantage.

News

- Jordan Nears Full Digital Government as 85.5% of Public Services Go Online

- Alphabet's AI Push Delivers Growth, but Spending Weighs on Cash Flow

- Saudi Arabia's AI Startups Outperform Global Counterparts, AWS Study Reveals

- OpenAI Models Breach Hugging Face Systems

- SDAIA Unveils AI Bias Guide, Identifies Over 100 Bias Types

- AI Adoption Doubles as Saudi Internet Penetration Reaches 99.6%

[Image: Chetan Jha/MITSMR Middle East]